Podcast Appearance: "Debt for the SaaS Masses"+ More Capital Provider Data

Perspectives and Quick Takes From Bigfoot and Our Community of B2B Software Operators and Investors

Happy Wednesday,

Welcome back to another edition of the Bigfoot Bi-Weekly Roundup.

This week I’m sharing:

A podcast I was recently on with some snippets below

A bit more data from our capital provider survey (investing activity)

A couple tweets I enjoyed

Cloud Returns Podcast: Debt for the SaaS Masses

Matt Harney of Cloud Ratings was kind enough to invite me onto his podcast. We dove into a variety of topics, including:

Access to capital in the current environment

Unique financing opportunities after disruptions like SVB

My perspective on the changing dynamics of whether to bootstrap + the increasing presence of VC in typically bootstrapped categories

Here are a few note-worthy areas we covered:

Being frivolous with equity

"I'm not anti the selling of equity in the life cycle of a company. However, as a lender who does not underwrite in a venture debt format, we want folks to show up who really cherish their equity. Now, we want this to be reasonable, as operators should realize that there are times and places within a company's life cycle to sell equity in service of some future outcome or growth profile.

What I’ve long taken issue with and what led me to start Bigfoot in the first place is the megaphone that VC has deployed against impressionable, less educated, less experienced operators. A lot of people over the past decade had the ability, sometimes unwarranted, unjustified or unnecessary, to go raise money by selling equity. I feel it became too much of an expectation and almost a requirement to have a “real” company. Folks should recognize what game they're playing, what game their counterparty is playing, what expectations there are on both sides and what limitations they may place on their company and its ultimate success.

What to know about BigFoot as a counterparty

What we're trying to do is run a nice, performant, efficient, lending business in our space. We’re not trying to hyperscale. We care a lot about the quality of our portfolio. We never want to overlever companies as we feel doing so reduces optionality both for them and for us. We certainly don’t want to manage the companies we lend to nor do we expect to own any piece of them. At the end of the day, we want to partner with operators who think about their businesses in a similar fashion as we think about ours - growth-oriented, not growth obsessed and with a long-term view to success, which requires sustainability.

Thinking Long term + Executing for the Near-Term

What's your North star? What are you indexing to? And how does that shift? 24-36 months ago, we were more heavily oriented towards growth. In our own company life cycle, we had proven to a degree, “hey we can put money out and have it come back.” The next thing to prove was that we could do that with some volume and pace. I feel we proved that. Then it was back to “can you manage a portfolio and continue clipping strong performance at that scale?” That’s where our focus has primarily shifted over the past 12 months, which frankly has been fine and appropriate in the market environment we’ve found ourselves in.

Capital Sentiment Survey - A bit more data

We wanted to share a few more data points from our capital sentiment survey that we released earlier this month, specifically as it relates to investment activity.

Investing Activity- All Equity Capital Providers

1H 2023 saw 40% of equity investors pick up pace relative to 1H 2022.

In 1H 2022, only 19% of equity investors were more active relative to 1H 2021.

Investing Activity - Equity Capital Providers by Stage

While Seed/A investors picked up their pace, ~50% of Series A/B/Growth investors were less active 1H 2023 vs. 1H 2022.

~2/3rd of all surveyed equity investors expect more investing activity over the next 12 months.

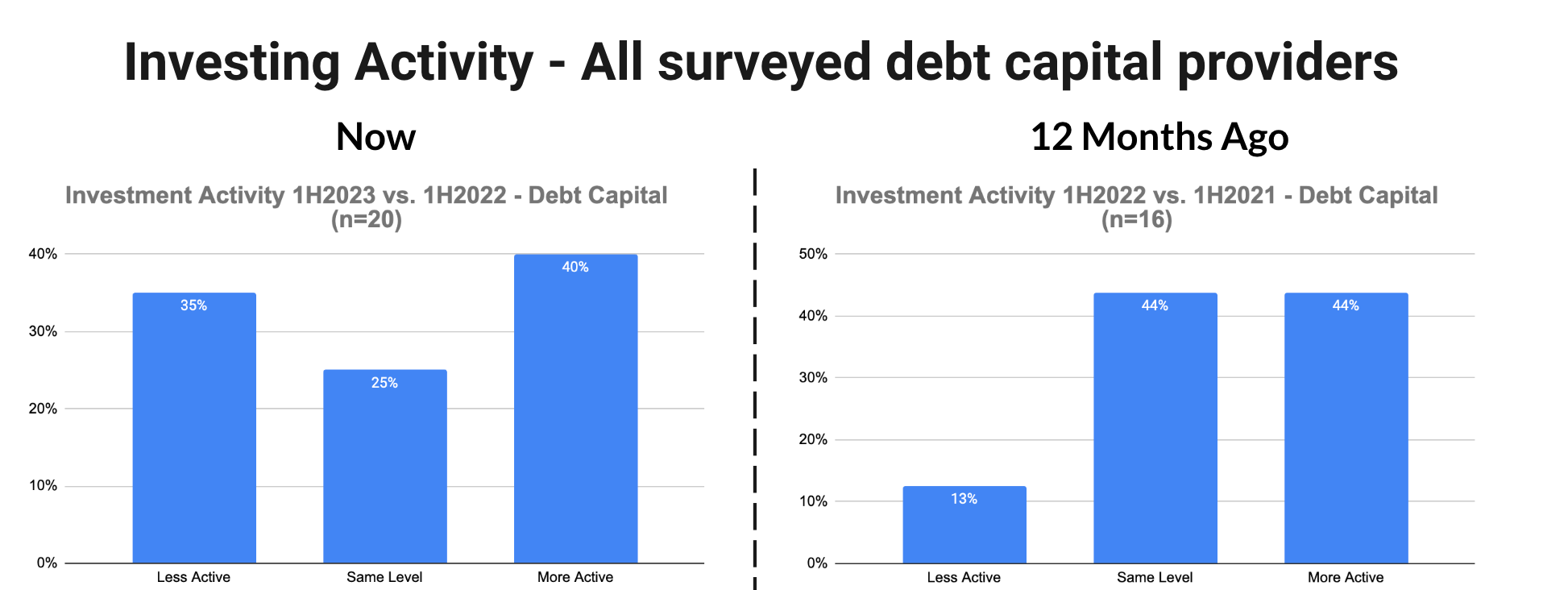

Investing Activity- All Debt Capital Providers

While a significant portion (40%) of lenders are more active YoY, we see a material shift to less activity from where it was 12 months ago comping YTD YoY (35% less active compared to 13% 12 months ago).

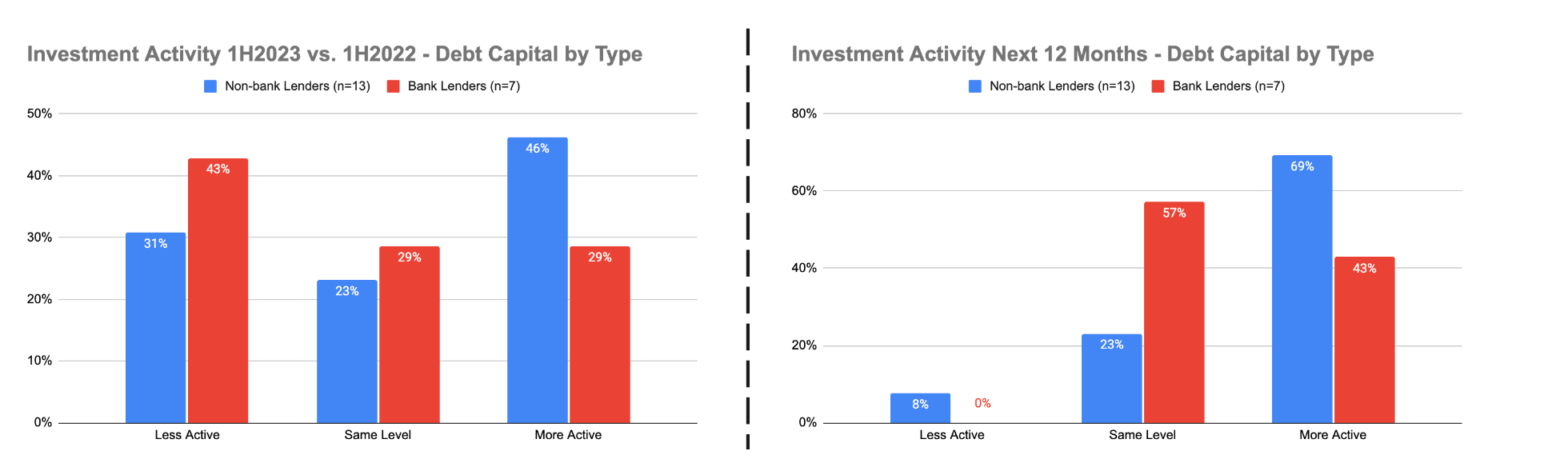

Investment Activity - Debt Capital Providers by Type

Unsurprisingly, non-bank lenders have picked up their pace and intend to keep doing so. Bank lending receded for obvious reasons in 1H2023 and has stabilized with a floor to grow from (at more reasonable levels).

You can find the whole report in this deck. Lots of charts, quotes, and comparisons.

🔊 Bigfoot Quick Takes 🔊

A Thread on Runway

I like the clear delineation between spend and investment.

Investments must be justified by returns delivered.

If those returns don't pan out, that "investment" is really just spending.

A lot of companies (and their investors) let that spending go on way too long.

Efficiency as a Cultural Trait

I really liked this take and agree that efficiency has to be baked into an operating culture and valued by all in the organization, starting with leadership. Of course, we’ve seen a massive move to operating efficiency over the past year+. A lot of companies have had to re-engineer their operating cultures to effectuate change. Hopefully, it sticks.

A question I have: will the current generation of tech workers carry this “cultural trait” of efficiency forward with them as they move up the org chart and start their own businesses? Time will tell.

About Bigfoot Capital

Bigfoot Capital offers growth-oriented loans for B2B software companies with $2M- $20M in revenue. We pride ourselves on partnering with companies and their stakeholders to provide a capital partnership that comes with stability and support.

If you operate or support a B2B software business and want to learn more about alternative capital options that preserve equity, get in touch with our team today.

Thanks for joining.

For later listening, all of the podcast platform links are included here:

https://cloudreturns.cloudratings.com/episodes/co-founder-and-ceo-of-bigfoot-capital-debt-for-the-saas-masses