VC/PE Exit Woes + A Decade of SaaS Data

VC/PE Exit Woes + A Decade of SaaS Data

Perspectives and Quick Takes From Bigfoot and Our Community of B2B Software Operators and Investors

Happy Wednesday,

Welcome back to another edition of the Bigfoot Bi-Weekly Roundup.

This week I’m sharing a bit on:

Private equity earning its illiquidity premium

SaaS Historical Benchmarks Report, using a decade of data

VC/PE LPs Feeling the Exit Freeze

“Where oh where could my exits be? The market took them away from me”

- VC/PE LPs

My wife and I watched Frozen with our 4-year-old recently for movie night. Elsa freezes up the harbor, trapping all the boats and thus the economy of the village. She didn’t really mean to, but she lacked control of her magic.

One can draw a parallel to what’s going on with frozen VC and PE portfolios and the assets trapped within them right now. The thawing is really outside of GPs’ control and will require some magic (or really just some movement) from the market. In the meantime, GPs and LPs alike are feeling it.

I ran across a “hmmm, interesting” private equity-related stat last week that further confirmed the lack of primary liquidity in PE portfolios (the same applies to VC).

I say primary liquidity with intent because now what we’re seeing is both PE and VC funds turning to secondary markets in an effort to get some cash back to their LPs. So far, this strategy hasn’t moved the needle, but maybe that will change.

In order for a true unthawing, there needs to be a big rebound in primary liquidity via the exchanging of assets b/t sponsors or with strategics. This must be paired with an at least ajar IPO window that doesn’t slam shut with a massive markdown of the assets coming through it, which would provide liquidity but would not generate real value.

Until we see these asset transfer mechanisms unlock, LP capital in VC and PE funds will remain there and returns for the asset classes will continue to degrade.

All this said, 2023 has been the most active year for acquisitions of companies in our portfolio since we started in 2017.

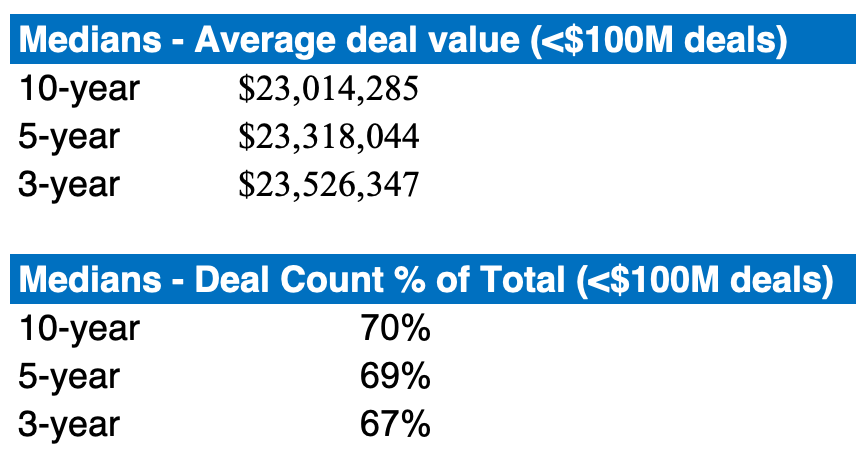

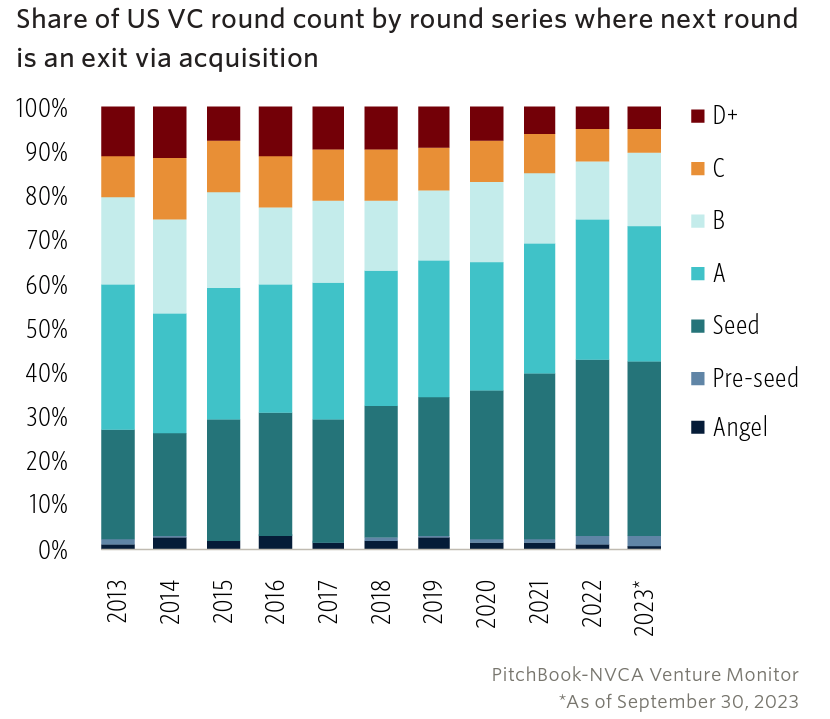

Given that 70% of PE deals are actually sub-$25M and 70% of acquired software companies are at the Seed or Series A stage, I suppose this makes some sense. See below so you know I’m speaking the truth.

*Source: Pitchbook Q3 2023 US PE Breakdown

Some Sweet SaaS Data

Matt Harney at Cloud Ratings continues to put out stellar content. He recently aggregated data from Pacific Crest/KeyBanc surveys conducted from 2010 to 2022 to procduce a SaaS Historical Benchmarks Report spanning over a decade.

Here a few takeaways:

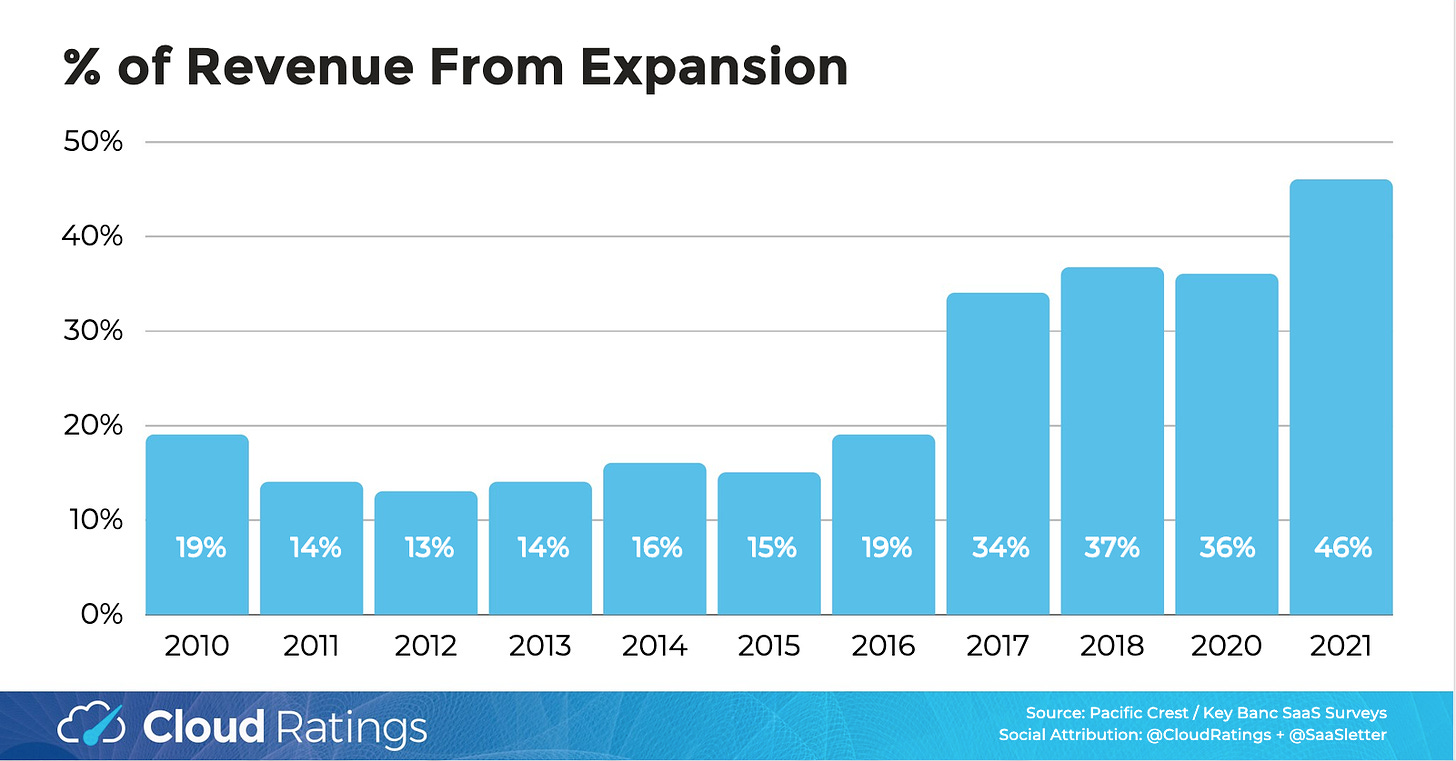

The contribution of Expansion Revenue continues to well…expand

I don’t know what happened in 2017 to drive a step change, but I’ll lift a point from Matt’s analysis.

“Installed base math: the early era of SaaS had definitionally a small installed base to expand upon. Whereas today’s SaaS vendors have decades of installed bases to expand from →that historic-to-new ratio imbalance mathematically will favor expansion as a driver.”

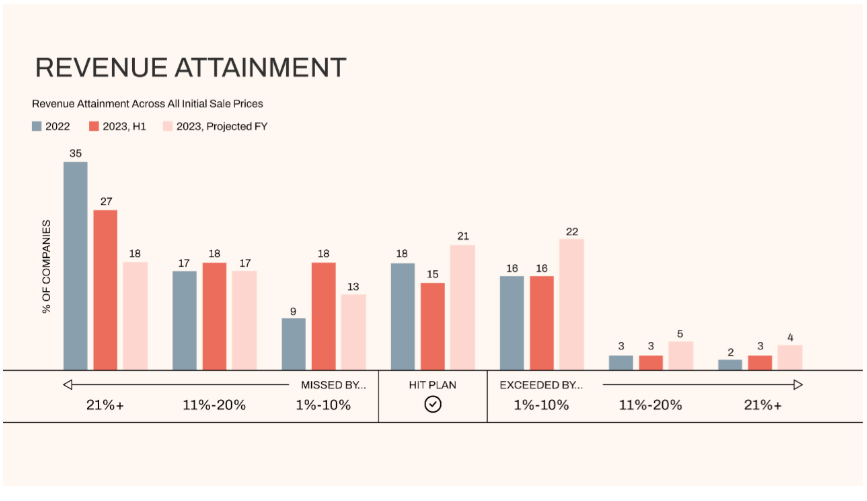

I like to think that I value expansion revenue as much as the next SaaS fan. That said, you’ve also gotta sell new stuff to new customers to have success, and that’s still hard slogging in the current environment (as conveyed in Lightspeed’s 2023 Sales Benchmark Report).

Only 37% of surveyed companies (n=143) hit or exceeded their revenue plan in 1H 2023, which pairs nicely with the fact that only 33% of sales reps hit 1H 2023 quotas.

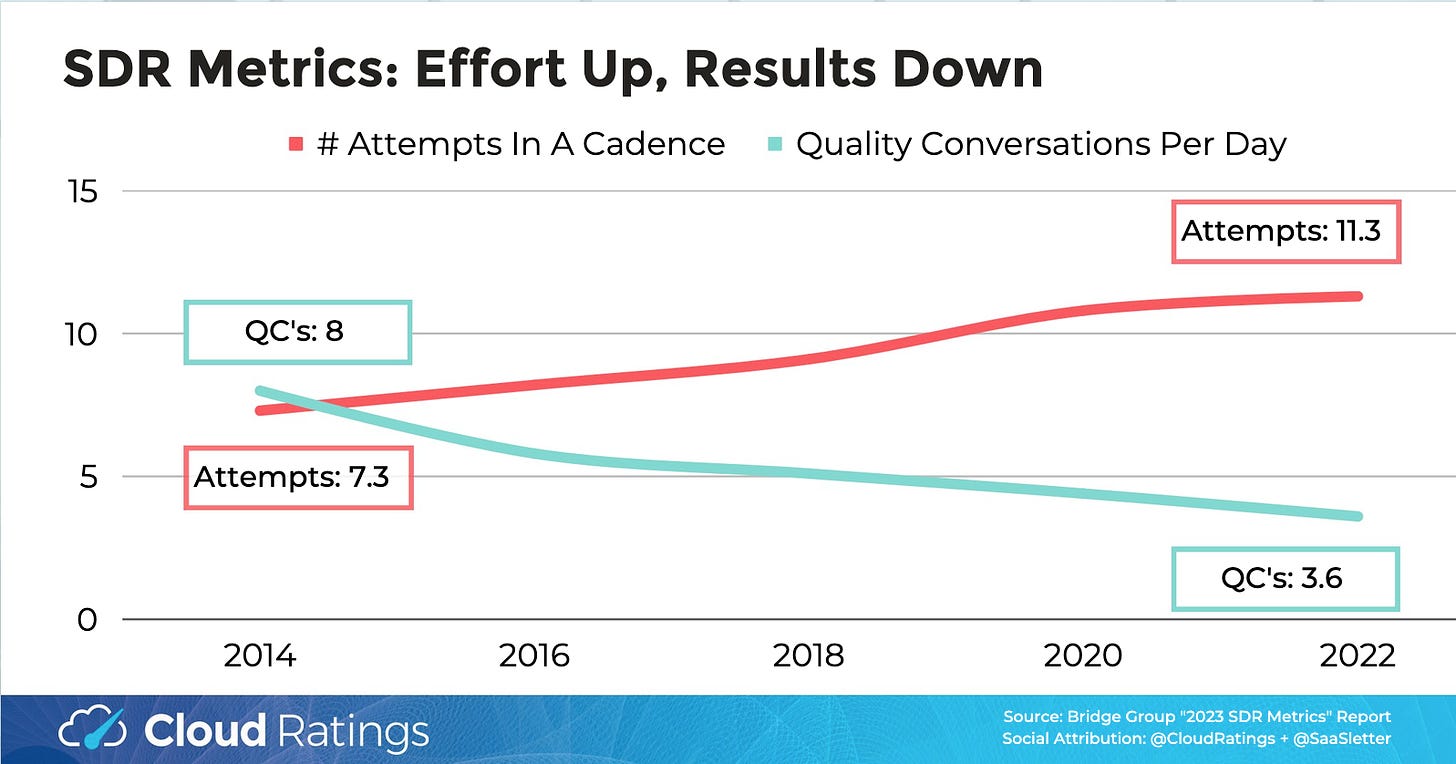

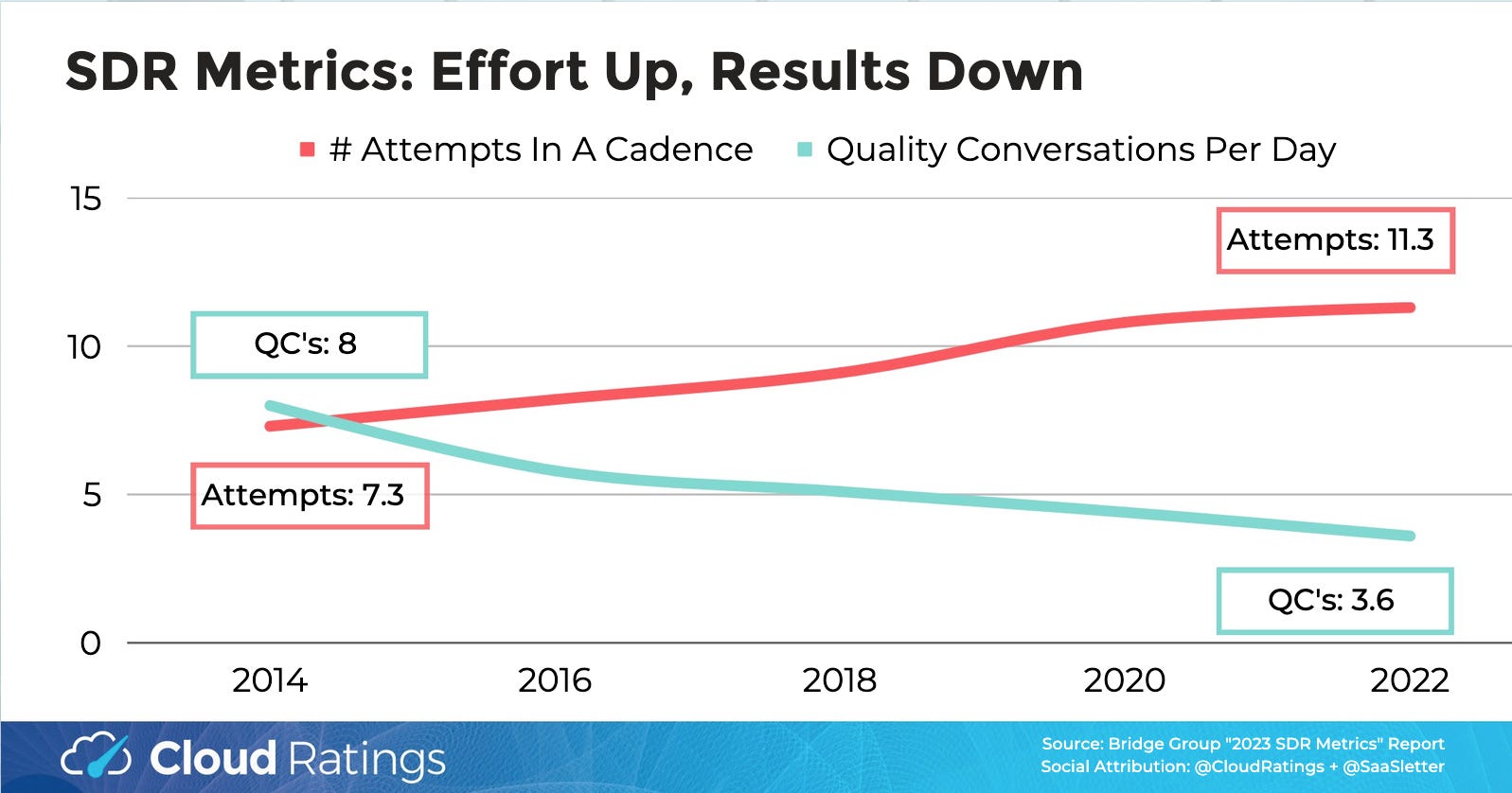

SDRs are throwing, they’re just not connecting

SDR quality conversations per day are down 55% from 2014 levels. An SDR is having 18 quality calls a week vs. 40 back then. That’s a BIG drop in top-of-pipeline productivity. Maybe we’ve all been dripped to death by now. Maybe, as software buyers, we’re over salespeople (survey says yes). I still root for solid SDRs.

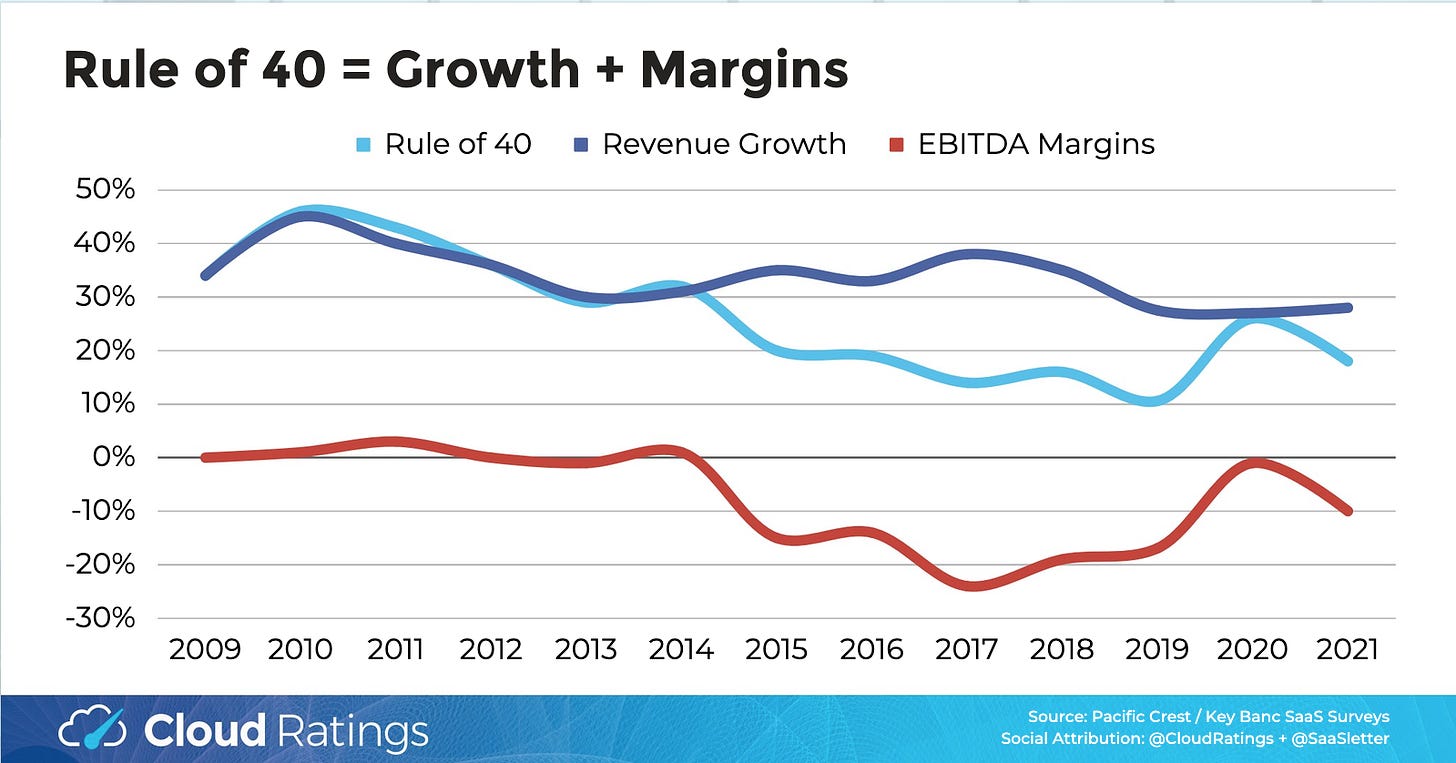

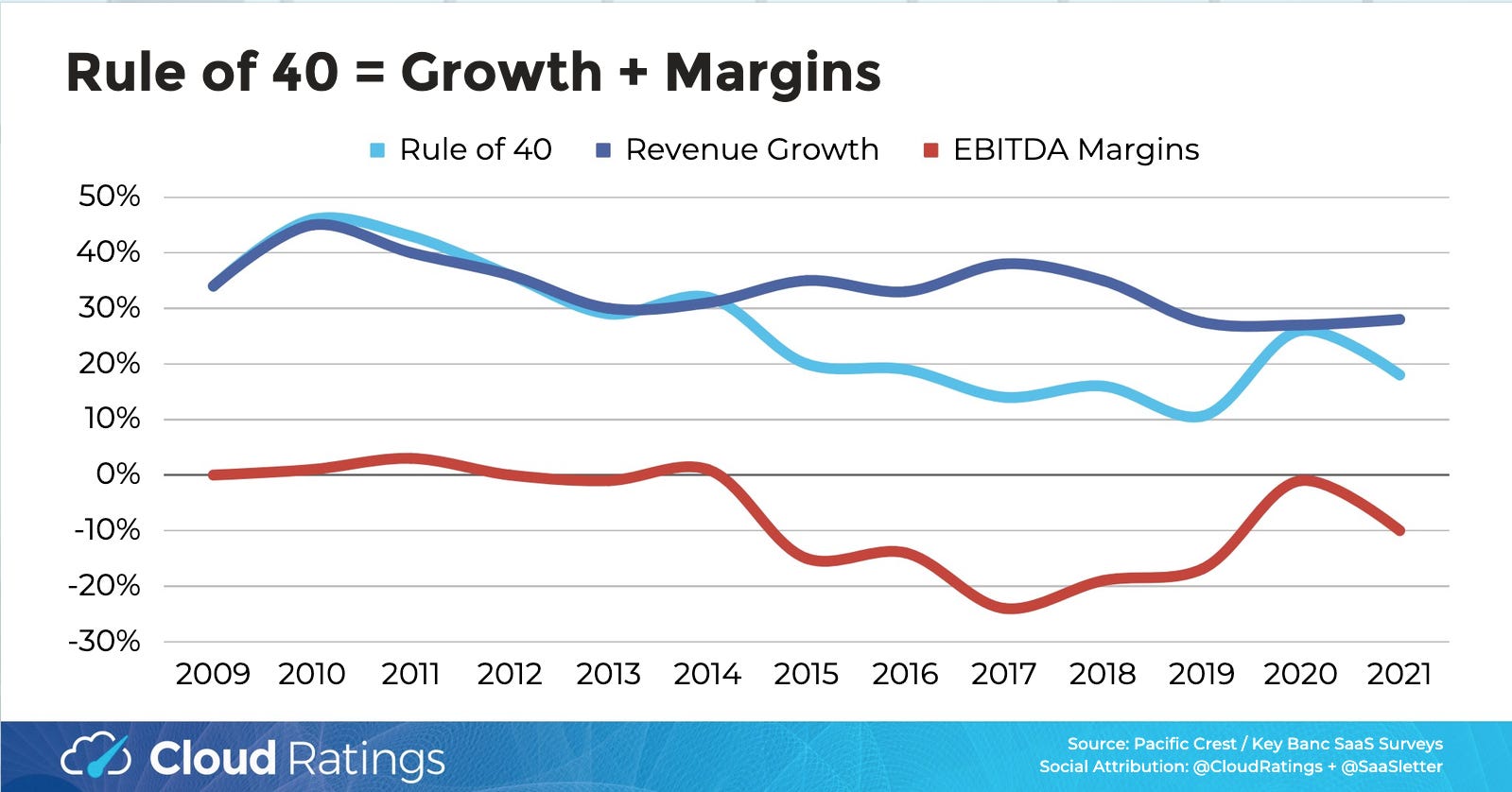

Rule of 40 schmorty

This is a pretty ugly slide both for growth and EBITDA margin. Up until 2015, software companies profiled in this survey were at least EBITDA neutral. Then, operational discipline and the conceptual value of cash flow seemingly went out the window, at the same time that growth was stagnating across the sample set. We’ll have to wait a couple of years to see what kind of rebound manifests with everyone’s march to efficiency.

I encourage you to check out Matt’s detailed write-up here and here’s the deck I sourced the slides from.

About Bigfoot Capital

Bigfoot Capital offers growth-oriented loans for B2B software companies with $2M- $20M in revenue. We pride ourselves on partnering with companies and their stakeholders to provide a capital partnership that comes with stability and support.

If you operate or support a B2B software business and want to learn more about alternative capital options that preserve equity, get in touch with our team today.